Finance 103 for Small to Medium-Sized Business Owners:

Understanding Business Cash Flow – Part II

This is the second installment of Understanding Business Cash Flow. In Part I, we discussed Cash Flow from Operations. This edition covers the remaining sections of the Cash Flow Statement:

- Cash Flows from Investing

- Cash Flows from Financing

"Many businesses fail because the owner wasn't willing to invest and wasn't educated on the difference between spending money frivolously and investing money into the business for growth, and the risks and rewards of that cash infusion."

– Carol Roth

Like spending for expenses, investing in capital expenditures requires cash. Consistent with the notion that a Cash Flow Statement is a bridge between the Income Statement and the Balance Sheet, the Cash Flows from Investing section focuses on those items that do not reduce income on the income Statement but they magically appear on the company Balance Sheet.

Cash Flows from Investing (1)

- All amounts are shown in red to reflect the fact that the items listed are a use of cash because they require a cash outlay.

- Capital Expenditures are usually investments in long-term assets such as equipment, buildings and land. Most companies will make capital expenditures every year. The ideal strategy is to have the income tax laws work in your favor by being able to deduct capital expenditures as depreciation on your income tax returns (at a faster rate than depreciation on your Income Statement). In this way, the income tax laws help you finance your equipment purchases.

- Small to medium-sized companies occasionally buy out minority shareholders.

When cash flow from operations is insufficient to finance the business, money must be obtained from external sources or from the owners. Typically, when the business has been established for some time, the company will obtain a line of credit from a bank. The funds obtained will be used to finance capital expenditures, fund working capital where accounts receivable or inventory needs to be financed or even, in some cases, to buy out minority shareholders or to pay off shareholder loans. In other cases, borrowing long-term may be available.

Cash Flows from Financing

- In this example, the company borrowed $240,000 on its line of credit over a 5 year period.

- These amounts represent principal payments on the company’s long term debt. Interest expense on their long-term debt, like all forms of interest expense, is shown on the company’s income statement.

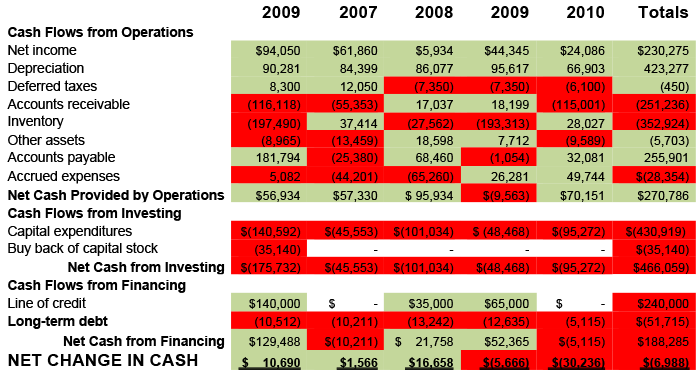

Now that we have looked at all the pieces of a Cash Flow Statement, here is a complete statement:

5-Year Cash Flow Statement

As you can see from the above example, over a 5-year period, the company had a small decrease in cash of approximately $7,000. Each year and each piece of the Cash Flow Statement generates a story about the business. For example, over the five year period, the company made the following investments:

- Capital expenditures – $430,919

- Inventory – $352,924

- Accounts Receivable – $251,236

These amounts total approximately $1,035,000.

It financed that investment primarily from the following sources:

- Line of credit – $240,000

- Accounts Payable (financing from vendors) – $255,901

- Depreciation – $423,277

The funds provided by these sources total approximately $919,000, with the remaining $126,000 provided from net income less the net effect of all other items not included here but shown on the Cash Flow Statement.

So, if you are wondering where your cash went, make sure you or your accountant prepares a Cash Flow Statement.

“There are lots of things that can be solved with cash.” – Danny Boyle

And, there is more, there always is.

Be genuine.

Copyright 2014 © John J. Trakselis, Chicago CEO Coaching

Join the Discussion

What’s on your mind? What’s keeping you up at night? What are the thoughts from your desktop? If you have topics you’d like John to cover in this blog, please email john.trakselis@vistage.com or call (708)443-5518.